How Mortgage Points Work, and When They're Worth It

Say the word "points" to someone shopping for a mortgage and you usually get one of two reactions. Some people hear it and assume it is a scam, a way for the lender to squeeze more money out of them. Others believe the opposite, that you should always buy points because a lower rate is always better.

Neither is true. Points are a tool. Like any tool, they are useful in some situations and a waste of money in others. Here is what they actually are and how to tell which situation you are in.

What points actually are

A point is prepaid interest. It is equal to 1% of your loan amount. On a $400,000 loan, one point costs $4,000.

When you pay that money upfront, you get a lower interest rate in return. That is the whole idea. You pay some interest now so you carry a lower rate later.

Almost everyone gets one thing wrong about points. People assume that buying one point drops your rate by a full percent, say from 7% down to 6%. That is not how it works. Buying one point usually lowers your rate by somewhere between an eighth and a quarter of a percent, depending on the lender and current market conditions. So one point might take you from 7% to 6.75%, not 7% to 6%.

Wait, isn't that what the Fed does?

You have probably also heard "points" used when the Fed talks about interest rates. That is a slightly different use of the word. The Fed moves rates in basis points, shortened to bps. One hundred basis points equals 1%. So when the Fed cuts rates by 25 basis points, rates should, on average, come down by 0.25%.

But something here confuses a lot of people. The Fed cuts rates, the news reports it, and then you call a broker for a quote and nothing has changed. Two reasons for that.

First, mortgage rates are not tied directly to the Fed. They follow the bond market, specifically the 10-year Treasury. The Fed influences that market, but it does not control it.

Second, the market prices in the Fed's decision before it happens. The big lenders setting rates already know what the Fed is likely to do, and they bake it into their pricing ahead of the announcement. There have even been times the Fed cut by 25 basis points and mortgage rates went up, because the market had been expecting a bigger cut.

There is no singular rate

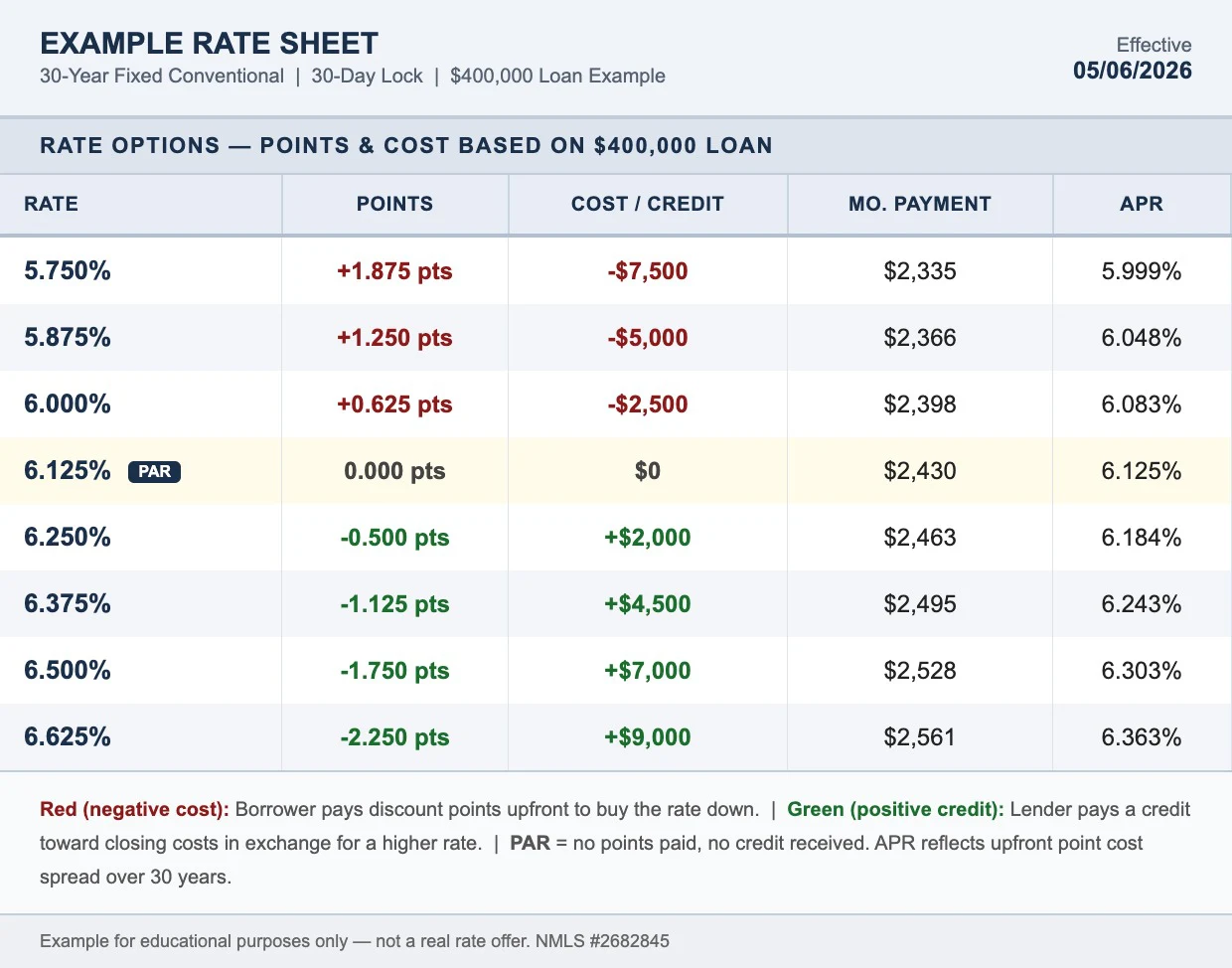

This is the part that ties back to points. Most people think there is one rate available to them based on their loan amount and credit score. There is not.

Lenders work off a rate sheet, and that sheet lists many rates, each with a different cost in points. The rate you usually see advertised is the one that costs zero points. Nothing extra to pay, and nothing paid back to you. That is called the par rate.

From there you have options. You can pay points to get a rate below par. Or you can take a rate above par and receive lender credits, where the lender gives you money to help cover your closing costs.

This is also why a Fed cut might not show up the way you expect. If rates improve, you might not see the exact interest rate drop. Instead you might see the cost of points improve. A rate that used to cost you money might now come with a credit.

The break-even math

Whether points are worth it comes down to one calculation. Here is an example.

Take a $400,000 loan with two options:

- Option 1: no points, 7% rate

- Option 2: one point ($4,000), 6.75% rate

On a loan that size, the gap between those two rates is roughly $65 a month. To find your break-even point, divide what you spent by what you save: $4,000 divided by $65 is about 61 months, a little over five years.

So if you plan to keep that loan and stay in that home for more than five years, buying the point can pay off. If you sell or refinance before then, you paid $4,000 and never got it back.

The Quote Comparison calculator runs this for you. Enter a couple of rate options with their point costs and it shows the true cost of each and where they break even.

When buying points makes sense

When rates are rising. When you buy points, the lower rate is yours for the life of the loan. If rates are climbing, there is little chance you will refinance into something lower later, so locking in a reduced rate now can be worth the upfront cost.

When your financial situation is about to change. This one gets overlooked. Even if rates are dropping, you might not be able to take advantage of it. Refinancing is not automatic. It is essentially qualifying for the loan all over again, with income, tax returns, and W2s. If you are about to go self-employed, take a gap in employment, or move to a lower-paying job, you may not qualify for that refinance down the road. If you expect to hold the loan a long time and a future refinance is uncertain, buying points to secure a lower rate now can make sense.

When it doesn't

When rates are dropping and your finances are stable. If you can reasonably expect to refinance into a lower rate within a year or so, spending a lot of money on points now is hard to justify.

When you are not keeping the loan long. If you are planning to move soon, or the home is a short-term place while you relocate for work, you will likely never reach the break-even point. The points just become a cost.

When you need the cash. If buying points would drain money you need for renovations, other expenses, or an emergency fund, that is a strong reason to skip them. Cash in hand has value too.

Bottom line

Points are a buy-now, save-later tool. You pay more upfront to pay less every month after that. They are not a scam, and they are not automatically smart. There is no universal answer that applies to everyone.

The real question is not "are points good or bad." It is whether the math and your own plans line up. How long will you keep this loan? Where are rates headed? Is your income steady? Answer those honestly and the decision usually makes itself.

If you are in North Carolina and want help running the points math for your situation, reach out and we can look at it together.

Watch: How Mortgage Points Work

Still have questions?

Browse the FAQ for quick answers, or get a free, no-commitment quote for your situation.