Why Did My Mortgage Change Hands After Closing?

You close on your mortgage with one company. A few weeks later, a letter shows up saying your loan has been sold or transferred to a company you have never heard of.

Did something go wrong? Is your rate changing? Why is this happening?

In almost every case, nothing went wrong. This is one of the most normal things that happens in the mortgage industry, and once you understand why, it stops being confusing.

There are actually four companies behind your mortgage

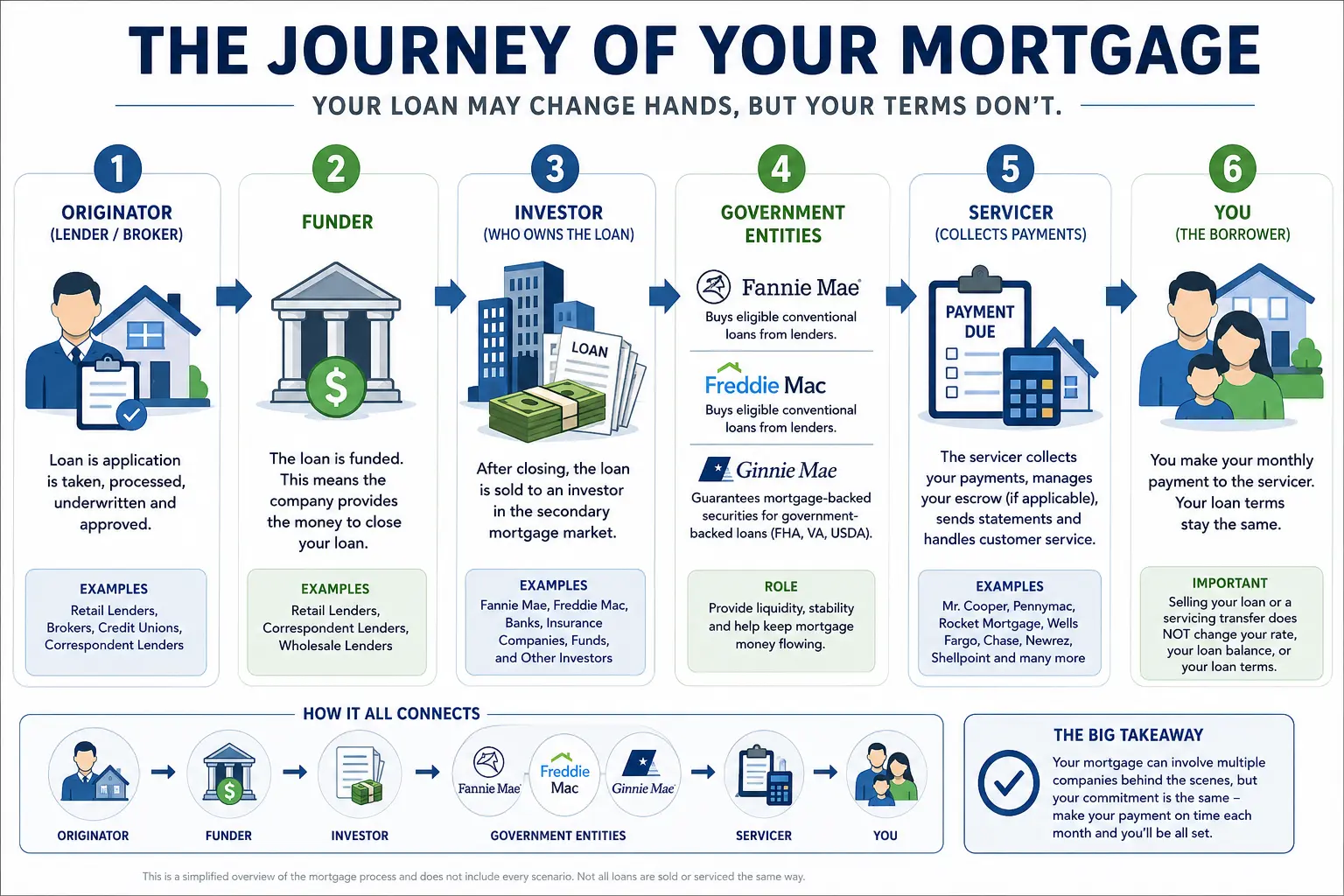

Most borrowers think of their mortgage as a relationship with one company. In reality, up to four completely separate companies can be involved, each playing a different role.

The originator is the company that helped you get the loan. They took your application, collected documents, worked with underwriting, and got you to closing.

The funder is the entity that actually provides the money at closing. In retail and correspondent lending, the originator and funder are usually the same company. In broker transactions, a separate wholesale lender funds the loan.

The investor is the company or institution that ultimately owns the loan. This is the entity that holds your loan as an asset going forward.

The servicer is the company you make your monthly payment to. They collect payments, manage your escrow account, pay your taxes and insurance, and handle customer service after closing.

Sometimes one company handles all four roles. Often they are different. And that separation is exactly why your mortgage can change hands after closing without your loan terms changing at all.

How mortgage companies are structured

Not all mortgage companies work the same way behind the scenes, and that structure affects how your loan gets originated and where it ends up.

Retail lenders have their own loan officers, operations, and underwriting under one roof. You work directly with them from application to closing.

Mortgage brokers work with multiple wholesale lenders behind the scenes. The broker manages your application and guides you through the process, but another lender funds the actual loan.

Correspondent lenders sit in the middle. They close the loan in their own name, often using a warehouse line of credit, then sell it to a larger investor shortly after closing.

Credit unions are member-based institutions that may keep loans in-house or sell them depending on their model.

None of these channels is automatically better or worse. They are different structures, and understanding them helps explain why your mortgage might move to a new company after closing.

What your loan officer actually does

One thing that surprises some borrowers: your loan officer is not personally funding your loan. They are also not personally setting the mortgage rates, and they are not deciding where your loan gets sold after closing.

Their job is to guide you through the process: structure the loan correctly, collect documentation, communicate with underwriting, solve problems, and get you to closing smoothly. That work has a significant impact on your experience, but it is separate from the pricing and capital decisions happening at the company level.

This is also why different lenders can quote different rates for the same borrower. Each company has different overhead, profit margins, investor relationships, and business models. The rate is not arbitrary, but it is not universal either. The right way to compare lenders is to look at the actual Loan Estimate: the rate, the loan costs, and whether there are points or lender credits involved. That is the only apples-to-apples comparison.

The secondary mortgage market

After closing, many mortgages get sold into what is called the secondary mortgage market. This is where lenders sell loans to investors after originating them.

The reason is capital. If a lender kept every mortgage on its books for 30 years, that is an enormous amount of money tied up for a very long time. By selling loans after closing, lenders free up that capital to make more home loans for the next borrower. It is how the system keeps moving.

This is especially true for correspondent lenders, which are companies that close loans in their own name using a warehouse line of credit, then sell those loans to larger investors shortly after. Selling the loan frees the warehouse line back up so they can keep operating.

Who buys these loans? Fannie Mae, Freddie Mac, and Ginnie Mae

The biggest buyers of mortgages in the secondary market are Fannie Mae and Freddie Mac, two government-sponsored enterprises that most people have heard of but do not fully understand.

They are not lenders you apply to directly. They operate behind the scenes, buying eligible mortgages from lenders, which frees up money so those lenders can keep originating loans. Without this system, it would be very difficult for lenders to offer long-term fixed-rate mortgages at scale. The 30-year fixed mortgage exists in large part because of this system.

Because Fannie and Freddie only buy loans that meet their specific guidelines, lenders have to verify that every loan qualifies before selling it. That is a big reason why lenders ask for so many documents during the process. They are not being difficult. They are making sure the loan will be eligible for sale on the secondary market.

Fannie Mae and Freddie Mac focus on conventional loans. For government-backed loans like FHA, VA, and USDA, a third entity called Ginnie Mae plays a similar role. Ginnie Mae works a bit differently: rather than directly buying loans the way Fannie and Freddie do, it guarantees mortgage-backed securities tied to those government loans. Because those loans carry government backing, they can sometimes offer more flexible qualification or favorable terms for borrowers who qualify.

What is mortgage servicing?

Servicing is the day-to-day management of your loan after closing. The servicer collects your monthly payment, manages your escrow account, pays your property taxes and homeowners insurance, sends your statements, and handles any questions you have.

Sometimes the company that originated your loan retains servicing. Sometimes servicing gets transferred to a different company. Common servicers include Pennymac, Mr. Cooper, Newrez, and Rocket Mortgage.

That transfer is usually what the letter in your mailbox is about. A new company is taking over as your servicer. Your loan terms do not change. Your rate does not change. The only thing changing is who you send the payment to each month.

Federal law requires that you be notified when your servicer changes. Your current servicer must send written notice at least 15 days before the transfer, and your new servicer must send notice within 15 days after. The notices will tell you who your new servicer is, when to start sending payments there, and who to contact with questions. During the transition, you also have a 60-day grace period where you cannot be charged a late fee if you accidentally send a payment to the old servicer.

The short version

If your mortgage changed hands after closing, it almost certainly means your loan was sold into the secondary market and a new servicer is now collecting your payment. Your rate, your term, and your loan balance are exactly the same. The only thing that changed is the address on your check.

This is how the mortgage industry has worked for decades. It is not a sign that something went wrong. It is the system functioning exactly as designed.

If you are buying a home in North Carolina and want to understand how your loan will be structured before you close, reach out. I am happy to walk you through it.

Still have questions?

Browse the FAQ for quick answers, or get a free, no-commitment quote for your situation.